Somewhere near two-thirds of American households subscribe to Netflix and Amazon—and these are just two examples of how the digital economy has become fully cemented in American life. From online grocery orders to digital content subscriptions, financial institutions (FIs) that offer payment cards are looking at increasingly lucrative opportunities to grab on to the coveted “top-off-wallet” position, making theirs the first card their account holders reach for when subscribing to digital services or making a digital payment.

Institutions that are successful in staking their claim to the top-of-wallet position in their account holders’ digital lives are likely to enjoy increased brand loyalty and stickiness alike—meaning not only are their cardholders more likely to reach for the FI’s card when setting up new payments, they may also be more likely to choose new products or services offered by the FI when considering their options in the future.

And these consumer habits translate into real income for FIs. With interchange revenue tied to FI card use, increased frequency of card use means higher revenue for the institution—and we all know that most Americans are only increasing their spend with digital merchants like Amazon.

Somewhere near two-thirds of American households subscribe to Netflix and Amazon

But how can FIs effectively obtain and maintain the sought-after top-of-wallet position? Loyalty or rewards programs may go some distance in elevating an FI card’s status, but there are unfortunately few—if any—digital solutions to address this opportunity, and most institutions lack the means of addressing this chance to build business and deepen relationships from a technology standpoint.

Interestingly, the best way to create the top-of-wallet benefits for FIs could be in solving a pain point for their end user.

Cardholder pain points and the top-of-wallet challenge

Financial institutions’ (FIs’) efforts to obtain top-of-wallet status for their payment cards can benefit their bottom lines and account holder relationships alike, by increasing interchange revenue and building brand loyalty. But how can FIs get to top-of-wallet more effectively? It could be as simple as providing a convenient solution for a common set of account holder pain points.

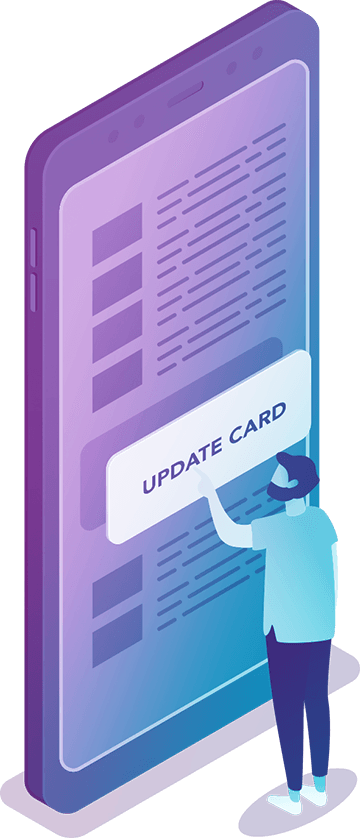

Think about this: with consumers’ increasingly widespread adoption of card-on-file services (e.g., Amazon, Netflix, Uber, and more) – any time you issue them a new card, you’re creating a pain point for them. This is because they have their old card stored, so when they get a new one, they have to undertake the painstaking process of going to every merchant they had their card saved, logging in, and entering their full card info—PAN, expiration, CVV—sometimes for as many as 10 or more merchants. So when a card must be replaced—whether due to loss, theft, expiration, or mass re-issue—an inconvenient cascade that can jeopardize a card’s already easy-to-lose top-of-wallet status ensues.

Staying top-of-wallet could be as simple as providing a convenient solution for a common set of account holder pain points.

As cardholders are forced to manually update their payment card information for all of their digital points of sale—Amazon, Netflix, bill payments, etc.—there’s no guarantee that their newly issued FI card will become their go-to payment method. Unless there are rewards or conveniences to be gained, the cardholder’s choice is likely arbitrary—and a profitable opportunity is lost for the FI. But what if you could provide an easy way for your account holders to manage this process in a simple, centralized way? By solving what is a manual and, frankly, crummy account holder experience, you might actually be able to incent the behavior you want out of your account holders.

Developing a new kind of response to cardholder pain points and the top-of-wallet challenge

There’s no question that getting your FI-issued debit or credit card to top of wallet represents a massive interchange revenue and account holder loyalty opportunity, but the fact is, few FIs have found a way to do this effectively.

Sometimes the best—and simplest—technology solutions are found at the intersection of user pain point and business needs.

When you issue a new card to an account holder, simply asking them to manually visit each merchant where they’ve stored a previous card and inputting their new card is not enough. At Q2, we believe that if you can alleviate what is a clunky, cumbersome process – manually updating your card on file across your favorite services—you can more effectively achieve top-of-wallet status (or maintain it where you already had it). Ultimately, the FI will have given their cardholders a reason to put their card top-of-wallet, garnering a number of possible benefits, including:

- Getting the FI’s card in use as broadly and frequently as possible

- Providing solutions that reduce pain points for cardholders

- Obtaining and maintaining the interchange revenue associated with the top-of-wallet card position

- Increased brand loyalty and brand stickiness, which may grow the likelihood of your institution maintaining its status as the primary checking and payment card provider for participating cardholders

Look at some of the ways Q2 is using open technology to address FI opportunities and gaps in cardholder services.